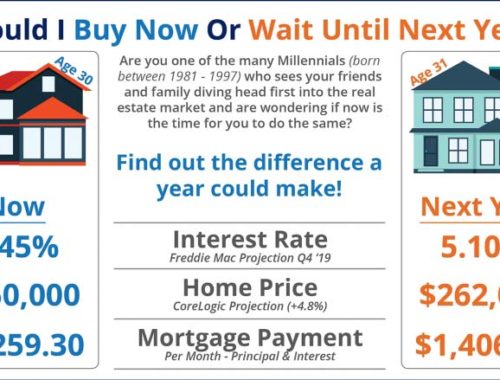

Appraisals – A Critical Part of the Transaction

With the tight market for buyers and the common practice of escalating up the offer price one savvy tactic for buyers is to offer, up front, to cover the difference if an appraisal should come low. Let me back up a bit here….

When a buyer takes out a mortgage, or when a homeowner refinances their home, the lending bank or entity will conduct an appraisal to verify the market value of the home. This protects the bank’s interest in the home and helps verify the percentage of equity the buyer or homeowner has or will have in the property.

It is important to know that when a buyer and seller agree on a price for a home, the appraisal may not reflect that same price. Especially in areas where prices have appreciated rapidly, it may be difficult for the appraiser to find comparable properties that have changed hands in the last three months which can help guide pricing on the current property. For example, say there were two comparable properties that sold four and six months ago in the area and in the last year, sale prices have gone up 15%. That means those two comparable properties may have sold for 5%-7.5% less than the property that is being appraised and the appraisal could be lower than the buyer and seller expect.

This is especially problematic in a transaction for two reasons:

- The appraisal represents the maximum the lender will lend on the property. So if an appraisal comes in at $300,000, the buyer and seller have already agreed on a price of $340,000, and the buyer is taking out a loan with 10% down, obviously the math no longer works. Depending on the agreement between the lender and the buyer, the lender may not be willing to loan more than 90% which would mean the agreed-upon price would need to be lowered or the buyer may need to put more money down.

- In the event the buyer is putting 20% down to avoid private mortgage insurance (PMI) (typically required when buyers or homeowners have less than 20% equity in the property) and the appraisal comes in low, then there is the potential problem of the buyer no longer having that 20% because some of the reserves may be used to make up the difference in the appraisal as in the following example:

- Agreed upon-price: $350,000

- Buyer is putting 20% down: $70,000

- Appraisal: $300,000

- Buyers and sellers renegotiate on price: $325,000

- Seller comes down by $25,000, buyer uses $25,000 of their $70,000 to make up the difference leaving them with $45,000 down payment which is only 15% of the loan, thus causing PMI to be assessed each month.

The bank may determine that the buyers have too many other monthly expenses to afford the PMI and denies the loan.

According to the National Association of REALTORS, in April of 2016, 12% of terminated sales failed due to appraisal issues which also led to delayed closings (28% of closings that were delayed were delayed due to appraisal problems). This is good information for you but I have the knowledge to help you navigate putting together a strong offer and negotiation that won’t get you in trouble with your loan.

You May Also Like