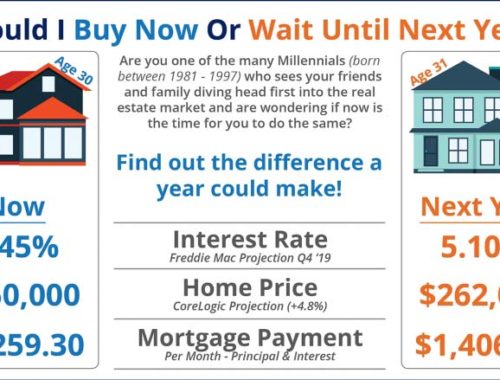

Interest Rates Heading Up? What You Need To Know

Interest rates are expected to rise over 2017 and they are already one the move. 30 year fixed-rate mortgage rates were as low as 3.42% as recently as October and up to 4.12% for the week ending January 12, 2017. That .7% rise may not seem like much, but for a loan of $200,000, at 3.42% the monthly principal and interest payment would be $889.18 and for 4.12% the corresponding payment is $968.72. That $79.54 difference over the life of the loan means another $28,634.40 in payments.

We have been spoiled by historically-low interest rates for years. But now that the economy is doing well, it is time for interest rates to head back up. The policies and investments proposed by the new administration that are meant to improve our economy even more may cause interest rates to creep up even further. It would not be surprising to see interest rates at 4.75% by year-end.

So what does this mean to you if you are buying or selling in 2017?

- First Time Homebuyer – If you are a first time homebuyer, the lower the interest rate, the higher your buying power. That being said, when interest rates are lower, there are usually more buyers in the market which means more competition. So you might have to pay more if you are competing with multiple offers. However, even when interest rates rise, there will still be buyers in the market – your competition, so your best bet will be to start that process sooner in 2017 rather than later.

- Selling – If you are just selling and not buying, then your best plan would be to set up a meeting with me to look at your options. There are different pools of buyers for each price point in the market and each is affected by interest rate changes differently. Will your property be affected by a change in the number of buyers or will competition still be high into the fall (at which point you may have seen greater appreciation on your home)? If this is your situation, let’s analyze it before you take action.

- Selling and Buying – If you are going to sell your home and buy another, depending on the interest rate you are paying now, the competition in the buyer pool for what you are selling and then the competition in the buyer pool for what you are buying (and how those are affected by a change in interest rates) it may be more advantageous for your transaction to happen earlier in the year, later in the year, or it may not make much difference. I would be happy to prepare an analysis on your home based on what you are paying now, what you could sell for now, and the financials for the home you are planning on buying both now and at the end of the year.

If you are paying less than 4% for your mortgage, it may be difficult to think about exchanging your low mortgage rate for a loan with a higher rate. However, if your current home is no longer serving your needs, there is value in your happiness. Let’s set up a free consultation to review your scenario and options. Call 206-370-0043 or email me at soldbyliznettles@gmail.com.

You May Also Like