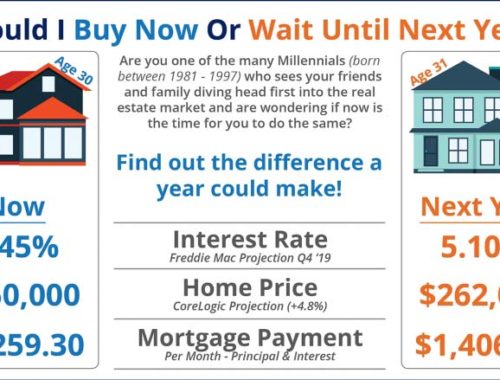

Mortgage Loans 101 – Part 2

Last post I talked about fixed and adjustable rate mortgages. There are additional terms that may be discussed and you may be wondering what the terms mean and how it applies to you.

In addition to the fixed rate mortgage and adjustable rate mortgages, mortgages may also be either “conventional” (meaning funded by the private sector – usually a bank) or a “government-backed” loan. Government-backed loans are backed by the federal government, including the Department of Veteran Affairs or the Department of Housing and Urban Development. The government agency is “insuring” the loan, although the funding may still be by a bank.

So why the two different types of loans? The Department of Housing and Urban Development typically has less-stringent lending qualifications, making it easier for some buyers to get a loan. For example, at the time of this writing, the down payment on an FHA loan (by the Federal Housing Administration) can be as low as 3.5% as opposed to a private loan which require 10-20%.

Below are the most-typical types of government loans:

FHA (Federal Housing Administration) Loan: The three benefits of this loan are the low down payment, lower credit score requirements, and additional monies to fix the home up can be included in the loan amount. Buyers who want to take advantage of an FHA loan first need to find an FHA-approved lender. I have a full list of our local FHA-approved lenders in the event these loan parameters sound like a good match for your needs.

Once the buyer finds a home and makes an offer, FHA will require an inspection of the property the buyer has made an offer on. There is a minimum list of requirements the property must meet in order for FHA to back the loan.

The drawback to an FHA loan? Government mortgage insurance is an additional expense you will need to cover.

VA Loan: These are managed by the Department of Veteran Affairs and are reserved for military service members. The benefit of a VA loan is it does not require a down payment. If you are a military service member, an agent can help you find a property, but when it comes time to apply for the loan, your Veterans Administration office will point you in the right direction and help you with the application process.

USDA Loan: These loans are managed by the United States Department of Agriculture and are reserved for rural areas. They are available to low-income residents. In our area, USDA loans may be available for the following areas outside the Seattle Metro area: Maple Valley, Kent, Carnation…

As you can see, there are pros and cons to both conventional and government-backed loans. If you are thinking about buying a home in the near future, let me set up a meeting with a lender who can guide you through the ins and outs of each, and help you determine the best loan for your needs and comfort level. Please contact me at 206-370-0043 or send me an email to elizabethn@johnlscott..com.

You May Also Like