What Does Taper Mean to Buyers & Sellers?

Taper means to diminish or reduce.

And why it’s important to the real estate industry right now is because the Fed again in January decided they were going to continue to taper. In December they decided they were going to start pulling back some of the stimulus that they had used in the housing industry. And remember what that stimulus did is it kept interest rates artificially low over the last few years. As they pull that stimulus back what’s going to take place is interest rates are going to start creeping up which every expert is saying is going to take place throughout 2014. But there’s another way to look at it, and I like the way Michael Deery, President of Citywide Financial Corp, looked at it. This decision from the Fed ‐ meaning to pull back on the stimulus and let interest rates start to rise ‐ is a trigger to get out there and look for a home while rates are low as the Fed is still giving buyers the opportunity to borrow money at a discount.

Probably the vast majority of you remember that interest rates before the government decided to get involved after the crisis were up in the 6, 6.5 percent range. Right now you can borrow money at 4.5 percent. That is a discount. You buyers have the opportunity right now to borrow money at a

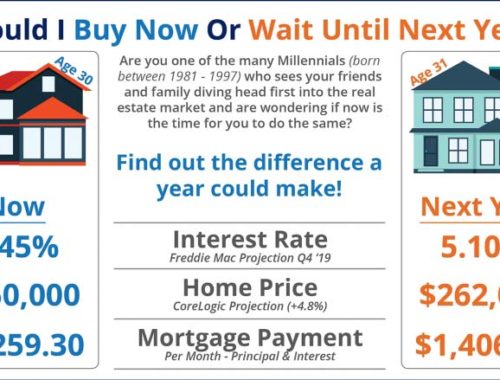

discount. Don’t pass that up. If we take a look at rates from 2013 all the way through the first couple of weeks of 2014, we can see that once the Fed even started talking about tapering rates jumped up dramatically toward the middle of last year; a full percentage point. And they’ve been bouncing around ever since. Most of the analysts believe ‐ and matter of fact each of the analysts actually project going forward ‐ believes that by this time next year interest rates will be over five percent. Still not a bad interest rate. I’m not saying that’s a bad interest rate. But when we’re looking at sub 4.5 percent interest rates today, that’s a big increase. And the National Association of Realtors believes that they’re going to go up a full percentage point from where they sit today.

See in December 2012 the average price, based on NAR’s average sales price, was $238,600.00. The interest rateback then in December 2012 was less than 3.5 percent so your principle and interest payment would be a little over a $1,000.00. If you waited until December 2013 ‐ well prices went up that year ‐ the new average price was $246,800.00 and interest rates jumped by more than a full percentage point. That means the difference in their monthly payment was $228.35 a month; over $2,500.00 a year. And over the 30 years of the loan we’re talking about them losing more than $80,000.00 in equity.

You May Also Like